CFPB's Payday Lending Rule

Payday Lending Rule

Although the Payday Lending Rule’s legal standing was in question for a time, the Supreme Court’s ruling in CFPB v. CFSA decided that the CFPB’s funding was constitutional and this law is slated to go into effect on March 30, 2025.

The Consumer Financial Protection Bureau's (CFPB) new Payday Lending Rule regulates how credit providers handle small balance, high interest accounts. It prohibits abusive practices like spamming payments to inflict overdraft fees, and requires lenders to notify borrowers before taking certain actions. This article will cover who it affects, what it requires, and how LoanPro can help you stay compliant.

Because of its thorny legal history, there is some confusion surrounding the rule. In 2017, the original Small-Dollar Rule was established, consisting of mandatory underwriting requirements and provisions on withdrawing payments from borrowers' accounts. In 2020, the Supreme Court overturned parts of the rule, and later that year, the CFPB released a revised Final Rule that removed the mandatory underwriting provisions. This new rule, the Payday Lending Rule, which takes effect in March 2025, still includes provisions on payments and customer communication.

What credit products are subject to the rule?

The Payday Lending Rule largely applies to (you guessed it) payday loans. Although individual states may define them differently, the CFPB set a definition in the regulation itself, (see §1041.3) which explains precisely which loans are covered by the rule and need to follow its requirements on payments, customer communication, and recordkeeping.

| Credit Product | Details |

| Short-term loans |

The first type of loan the rule covers are short-term loans. While other federal or state regulations might draw the line differently, the rule says that it's any closed-end credit where the borrower has to pay back "substantially the entire amount of the loan within 45 days," (§1041.3(b)(1)). The regulation is somewhat vague as to what "substantially the entire amount" means — the official interpretation notes that whatever substantial means "depends on the specific facts and circumstances of each loan". |

| Longer-term balloon-payment loans | Even if a loan has a term longer than 45 days, it can still be subject to the rule if the loan schedule includes a "balloon payment". A balloon payment is either a single payment for the entire loan amount, or any payment that's twice as large as any other (§1041.3(b)(2)). This might include a loan where the borrower has the option to make only minimum payments until a specified date when their remaining balance all comes due at once. If that final payment would be more than twice the size of the minimum payments, then the loan is subject to the rule (§1041.3(b)(2)(ii)(B)). |

| High-cost longer-term loans |

For these loans to be subject to the rule, the lender would need to meet the requirements of having both an APR of 36% or higher and a "leveraged payment mechanism". This goes for both closed-end and open-end credit. For open-end credit, this condition is met if the APR reaches 36% during any billing cycle or any time there is a balance of $0 and the lender imposes a finance charge. If an open-end credit meets this condition at any point, it is subject to the rule for the rest of the plan's duration. However, credit cards are an exception, as detailed below. What is a "leveraged payment mechanism"?A leveraged payment mechanism is any means of a lender initiating the transfer of money from a borrower's account (§1041.3(3)(c)). For instance, ACH and bank card transactions in LMS are leveraged payment mechanisms because you have the borrower's payment profile saved and can initiate a payment without any input from the borrower. The official interpretation explains that there are multiple ways the lender can withdraw funds from a borrower's account, such as check, electronic fund transfer, created checks/payment orders, and the transfer by an account-holding institution. |

Loans that are not covered by the Payday Lending Rule initially can become a covered loan at any time during the loan's term if it meets the criteria at a later point due to extensions or increased cost of credit.

What credit products are not subject to the rule?

If a loan doesn't match any of the three criteria above, it's not covered by the rule and you don't need to worry about any of the regulations, end of story. But for loans that appear to match, there are also some exceptions for certain types of loans. Even if the loan meets the above criteria, the following types of loans are exempt.

| Credit Product | Details |

| Certain purchase money security interest loans | "Certain purchase money security interest loans" are exempt from the rule (§1041.3(d)(1)). These are loans where a lender extends credit to a borrower for the sole purpose of purchasing a good, which is then used as collateral. If the borrower fails to pay back the loan, the lender repossesses the collateral item. Basically, the CFPB trusts that if you have the option to repossess the collateral, you'll do that instead of repeatedly attempting charges, so you're exempt. The official interpretation states that the loan is "made "solely and expressly" for purchasing a good if the loan amount is "approximately equal to, or less than, the cost of acquiring the good." So, an auto loan, or any other loan where buying the collateral item is the main purpose of giving credit, is exempt from the rule. But a loan for $1,000 with a $300 collateral item would still be subject to the rule. |

| Real estate secured credit | This rule does not apply to any loan that uses real estate as collateral (§1041.3(d)(2)). If the lender records or perfects the property with a lien in the loan contract, the loan is exempt from the rule. The law states in the interpretation that "if the lender does not record or perfect the security interest during the term of the loan, the credit is not excluded" and the loan would still be subject to the rule. It also clarifies that any personal properties that are used as a dwelling, like a mobile home, fall under the same category and are likewise exempt. |

| Credit card | Regardless of the interest rate or term, any open-end (not home-secured) credit cards are exempt from the rule (§1041.3(d)(3)). For specific details on what counts as a credit card, see Regulation Z. |

| Student loans | Student loans and private education loans are exempt from the rule (§1041.3(d)(4)). For more specific details on what education loans are exempt, see Regulation Z and Higher Education Act. |

| Non-Recourse Pawn Loans | The rule makes an exemption for pawn loans where the lender has physical possession of the pawned item for the entire length of the loan. (§1041.3(d)(5)). The interpretation makes it clear that these loans are only exempt if selling the pawned item is really their only recourse when borrowers fail to repay: If any borrower or co-signor "is personally liable" for a difference between the remaining loan balance and the value from the pawned item, then the loan is still subject to the rule. |

| Overdraft Service and Lines of Credit | An account-holding institution like a bank or their partner might extend an overdraft line of credit to their consumers. If their account lacks funds for a transaction, the bank would use the overdraft credit rather than charging an overdraft fee (which would help consumers avoid late fees from whoever initiated the charge). Overdraft services and overdraft lines of credit are exempt from the rule (§1041.3(d)(6)). The official interpretation points lenders toward 12 CFR 1005.17(a), where they can find a more thorough definition for these programs. |

| Wage Advance Programs |

A wage advance program, as explained in the Fair Labor Standards Act, is where an employee requests payment from their employer before the end of a pay period. Wage advance programs are exempt from the rule if they meet two requirements:

|

| No-Cost Advances | No-Cost Advances are loans where the lender agrees in the loan contract that if the borrower does not repay, the lender has no claim against them (§1041.3(d)(8)). The lender will not be involved in any debt collection activities such as selling to a third party or reporting to a credit agency. These loans are exempt, which is funny, because the lender by definition wouldn't be involved in any of the regulated activities like repeatedly charging an account. |

| Alternative Loans |

Alternative loans are similar to a payday loan, but are extended by a Federal Credit Union and meet certain conditions relating to the loan terms and underwriting. This is all laid out in another set of regulations, 12 CFR 701.21(c)(7)(iii). The definition for alternative loan is very involved, but any loan that qualified under §701.21 has safe harbor here and is exempt from the rule (§1041.3(e)). Conditional requirements for alternative loansLoan Term Conditions:

Borrowing History Condition:

Income Documentation Condition:

Safe Harbor:

|

| Accommodation Loans |

These are accounts that would normally be subject to the rule, but the CFPB has extended you a bit of leniency if you have relatively few of them (§1041.3(3)(f)). At the time of the loan being created, these loans are exempt if they meet both of these conditions:

|

Requirements and LoanPro solutions

To stay compliant with the three new primary requirements of the payday lending and small-dollar rules, LoanPro has implemented these solutions:

- Safeguards against submitting payments that will fail and tracking of failed payment attempts

- Automated communication of notices

- Compliant document storage and record keeping

LoanPro doesn't completely implement these solutions by default, but the sections below will go over what the new small-dollar rule says, and how to configure LoanPro to help you with compliance.

Requirement 1: consecutive failed payments

The rule requires lenders to get a written reauthorization to use a payment profile (i.e. a specific card or bank account) if two consecutive unsuccessful payment attempts are made with that profile. Many companies and legal minds have interpreted this to include both bank accounts and debit cards.

The purpose of this is to prohibit attempting to charge an account that has repeatedly lacked funds (see §1041.8(b)), so borrowers don't continue to receive overdraft fees on their accounts. If a payment profile has two consecutive transactions fail because of insufficient funds, a lender is legally restricted from trying that payment profile again unless and until they get reauthorization from the borrower. The restriction takes effect as soon as the lender or their agent (such as a payment processor) receives notice of a second failed payment.

The rule's two consecutive failed payment criteria are met when there are any failed transactions using the payment profile for a loan covered by this rule. This means that if a borrower has multiple covered loans with the same lender, which use the same payment profile to make payments, the requirement is triggered by any two consecutive failed payments on that payment profile, even if the payments failed for two different covered loans. It does not, however, include any failed payments for loans not covered under the rule.

Solution: LoanPaymentPro pre-transaction verification

The best way to comply with the consecutive-payments portion of the rule is to avoid consecutive failed payment attempts. This may not always be possible, so it is also important to have a way to detect failed transactions for a payment profile.

The easiest way to avoid consecutive failed transactions is never to submit a transaction that will fail. This may not seem helpful, but lenders usually have an understanding of their customers, and some information on payment history. If you have used a payment profile in the past that has a high failure rate, think twice about attempting a payment using that profile. Use information you have to set up pre-scrubbing to avoid submitting high-risk transactions. If possible, keep multiple payment profiles on file for problem accounts.

This feature lets you verify that funds are available for a debit card transaction before you attempt to process a payment. Here are the steps you need to take to use this feature.

- If you haven't already, sign up to use LoanPaymentPro as a payment processor. (Our support team can point you in the right direction.)

- Create a Secure Payments LoanPaymentPro bank card processor.

- Turn on the pre-transaction verification feature.

With pre-transaction verification, you will never be in danger of any failed payment attempts. This verification double checks that there are funds in the borrower's account before actually charging them.

LoanPaymentPro configuration details

Our article LoanPaymentPro gets into the details and explains how to turn this feature on.

Lenders who use LoanPaymentPro (LPP) as a payment processor can choose to enable a pre-transaction verification. While LPP can process both ACH and bank card transactions, this option only works for card transactions. This option sends out a verification prior to each transaction that ensures there are sufficient funds in an account before any withdrawal attempts are made. This verification double-checks the borrower's account information and will prevent you from trying to pull funds if they aren't there. If funds are present, the payment will be completed. You won't have to worry about failed payment attempts, and your borrowers will appreciate that they aren't getting hit with overdraft fees.

Solution: NACHA multiple returns

If you can't prevent those failed payments, the next best solution is an automated system that stops future payment attempts. NACHA has a built-in-system that can automatically prevent payment attempts when more than one payment has failed. NACHA notifies you of any failed payment attempts which informs you if you can charge that same account again.

This feature keeps track of failed payment attempts and lets you specify what to do when failures happen. This feature only works with NACHA payments. Here are the steps you need to take to use this feature:

- Configure the LMS Multiple Returns Feature.

- Process payments through a Secure Payments NACHA processor.

- Upload the returns file from the batch of payments to Secure Payments.

NACHA configuration details

If you process payments through NACHA, failed transactions will be returned along with return codes indicating why payments failed, such as insufficient funds, an invalid bank account number, or the account being closed. In LMS, our Multiple Returns tool lets you use those return codes as triggers for automated responses.

You can set up a rule-based action in Multiple Returns that will inactivate a payment profile the instant you receive two consecutive returns. You could even set it to inactivate the first time you receive a failed return in order to avoid getting a second consecutive return in the first place. If you do end up receiving two consecutive failed returns, you can also set up a trigger based notification that will automatically send the required Consumer Rights Notice, covered below. These two actions can even be linked by setting the multiple returns action to send a loan to a specific portfolio that is tied to a trigger based notification.

If you don't use LoanPaymentPro or NACHA Multiple Returns, we encourage you to speak with your payment processor to see what they can do to help you track or avoid consecutive failed payments.

Requirement 2: required notices

The new rule requires companies to provide their borrowers with notices under three different circumstances:

- The first withdrawal made by the lender

- Anytime the payment is considered ‘unusual’

- When two consecutive failed payments occur.

All of these notices must be formatted according to the Small-Dollar Rule's specifications.

Small-dollar rule disclosures

The Small-Dollar Rule specifies that all disclosures must meet specific criteria (see §1041.9(a)). Some of the criteria are common sense; the communication has to be clear and conspicuous, with the location and font readily noticeable, and the message needs to be readily understandable. It also needs to be

Delivered in writing, whether it is physically or electronically, in a retainable form. A retainable form is either a physical copy, or a digital copy that can be saved, downloaded, or emailed.

Segregated from any other communication. (This means that other information cannot appear above, below, or around the notice. It can, however, appear in a separate sheet of paper or a separate webpage.)

Available in English upon request, but can be sent in a language other than English.

Electronic disclosures

In order to send disclosures electronically, the lender must obtain the borrower's written consent. Lenders are also required to have an available email option, separate from mobile apps or text messages. A borrower's consent to receive electronic disclosures can be revoked by the borrower at any time through any means of communication, including: phone call, mail, text message, email, or an 'unsubscribe' link. Consent is also revoked if the lender finds out that the borrower is unable to receive disclosures through that method. (If there is a bounced email notice, a message from the borrower indicating that they can't access the communication, etc.) Finally, disclosures must be machine-readable; in other words, they must use machine-readable text that is accessible via both web browsers and screen readers.

Consent must be obtained for each method of electronic delivery, and borrowers must be given the option to select a particular method of electronic delivery. A checkbox during a borrower's origination process can count as written consent.

Sending electronic short notices through SMS or other applications

If a lender chooses to send a disclosure through a mobile app or text message, an Electronic Short Notice is required ( see §1041.9(b)(4)). The short notice is basically a way to send basic information included in the notice with a link to a retainable form. If the notice is delivered by email, an electronic short notice is not required as long as the full notice is delivered in the body of the email. If an emailed notice is provided as an attached PDF or linked URL, the electronic short notice is required and needs to be provided in the body of the email. All electronic short notices need to contain the following information:

- Identifying statement

- Transfer terms (including the date, amount, and borrower account)

- Website URL (linking to the full notice)

And just like the full notices, an electronic short notice sent in regards to an unusual withdrawal needs to explain what makes the withdrawal unusual:

- Varying amount

- Date other than the regularly scheduled date

- Different payment channel

An electronic short notice for consumer rights notice (see §1041.9(c)(4)(i)) also requires additional information, including:

- Disclosure that the last two withdrawal attempts were returned

- Borrower account information

- Statement of Federal law prohibition

There are not any requirements for what order this information needs to be displayed in for the electronic short notice.

First payment withdrawal notice

A lender is required to give a First Payment Withdrawal Notice (see §1041.9(b)(2)) after they obtain payment authorization (the information needed to withdraw the payment), before the first withdrawal. If a borrower provides a first payment in cash or a single immediate payment transfer, the First Payment Withdrawal Notice will not be given until authorization for a withdrawal is made for the first time. Once the First Withdrawal Notice has been given, the lender does not need to do so again even if the borrower makes an unscheduled intervening payment.

When should the notice be sent?

The earliest point that a lender can provide the First Payment Withdrawal Notice is when the lender first obtains the payment authorization (the information to withdraw the payment). The latest the notice can be given is dependent on whether the notice is sent by mail or electronically. The notice can be sent one of three ways:

In Person – Notice must be provided no earlier than when the lender obtains the payment authorization and no later than 3 business days prior to initiating the transfer.

Mail – Notice must be sent (placed in the mail) at least 6 business days before the withdrawal.

Electronic Delivery – Notice must be sent 3 business days prior to initiation of the transfer.

Unusual withdrawal notice

Notice must be of unusual withdrawals (e.g. withdrawal on a date other than the scheduled payment date), prior to attempting the transaction.

When is a withdrawal considered unusual?

Varying Amounts – If the withdrawal will be for an amount different from the regularly scheduled payment, the notice will need to include both the amount of the payment and whether it's greater or lesser than the norm.

Varying Dates – If the payment comes on a date that isn't part of the regular schedule, the notice should include the date for the payment.

Different Payment Channel – If you're using a payment method different from the one used in the previous payment (i.e., a different payment profile,) this notice will note that you're processing it through a different method.

Re-Initiating a Returned Transfer – If you're retrying a failed payment, this notice should include “the date and amount of the previous unsuccessful attempt, and a statement of the reason for the return.”

When should the notice be sent?

The timing of the notice varies based on how it is delivered.

In person – If the notice is provided in person, it should be provided no earlier than 7 business days and no later than 3 business days prior to initiation of the transfer.

Mail – If the lender sends the unusual withdrawal notice by mail, it must be mailed no earlier than 10 business days and no later than 6 business days prior to initiation of the transfer.

Electronic Delivery – If the lender sends the unusual withdrawal notice through electronic delivery, the notice must be sent no earlier than 7 business days and no later than 3 business days prior to initiation of the transfer.

Consumer rights notice

The Consumer Rights Notice (see §1041.9(C)) is required any time that the lender has initiated two consecutive failed payment transfers from a consumer's account. The lender is prohibited from initiating any further payment transfers until further authorization has been obtained. A payment transfer is deemed to have failed when it results in a return indicating that there are insufficient funds.

Account holding institutions

If the lender is the consumer's account-holding institution (such as a banking institution that holds both the borrower's checking account and loan account), a payment transfer is deemed to have failed any time the account lacks sufficient funds to cover the payment amount. (This means the lender doesn't need to receive a return stating the account lacks sufficient funds in order for the notice to become a requirement if the account lacks sufficient funds for two payments in a row.)

When should the notice be sent?

The requirement is triggered anytime information is provided to the lender or its agents that a second consecutive payment transfer has failed. The lender must send the notice no later than 3 business days after the second consecutive payment transfer has failed. This timing applies regardless of the method of sending the notice (by mail or electronically).

The lender cannot request authorization for additional payment transfers until the Consumer Rights Notice has been sent. A lender can send a request one of three ways:

Through letter communication (by sending it in the mail or giving it in person)

By email (if the borrower has given written consent)

By phone call (this only applies if the consumer contacts the lender in response to the consumer rights notice and agrees to receive the terms and statement in that same phone call). A retainable form must be sent if authorization is received by phone call.

Solution: LoanPro notification solution

LoanPro LMS has a notifications feature that will let you set up each required notification, so that the notification will be sent out automatically at the correct times. We have created custom forms templates for the notices that lenders are required to send. These are explain and available to download at the end of this article under ‘Notice Templates’.

How LMS automated notifications work

Since there are specific criteria that need to be met in regards to the templates and formats used for each of these notices, LoanPro has prepared forms that follow the rule's safe harbor templates. Every lender is able to access these notification forms in CFPB Small-Dollar Rule Templates. The process of sending the notifications can also be automated through the LMS trigger-based notifications feature. You can set your triggers to automatically send the notifications in the required time frame by mail, email, or text message (see electronic short notice requirements in section 3.6). Once these trigger-based notifications are set, you never need to worry about compliance to notification requirements because the process will be completely automated.

If you don't want the process to be completely automated, you can also use trigger-based notifications within the system to notify your agent user, and you have the option to create your own notification templates through custom forms. The rest of section 3 will go over the specific notifications and their requirements.

Requirement 3: compliance and record keeping

Compliance program

Lenders are required to create a compliance program by developing written policies and procedures (see §1041.12(a)). The purpose of this compliance program is to provide guidance to lenders' employees on how to comply with the requirements; as such, the procedures and policies need to be appropriate for the size and complexity of the lender and its affiliates, as well as the nature and scope of their covered lending activities.

Record keeping

There are a few considerations related to Small-Dollar Rule record keeping. All records related to the loan, including transaction history and authorization, need to be kept for the entire life of the loan and at least 3 years after the loan is no longer outstanding, and there are some documents that need to be retained specifically in tabular format.

What is tabular format?

Tabular format means that the "individual data elements comprising the record can be transmitted, analyzed, and processed by a computer program, such as a widely used spreadsheet or database program. Data formats for image reproductions, such as PDF, and document formats used by word processing programs are not tabular formats" (§1041.12(b)(5) interpretation).

Record-keeping details

In order to keep evidence of compliance, lenders must retain documentation for 36 months after the date when a covered loan ceases to be an outstanding loan (see §1041.12(b)).

Records that must be retained physically or by reproducible image:

- Loan agreements for each covered loan

- Leveraged payment mechanisms (bank accounts, bank cards)

- Authorization of additional payment transfer

- Underlying one-time electronic transfer authorization or underlying signature check

Records that must be retained electronically in tabular format:

- Date payment was received or payment transfer was attempted

- Amount of payment due

- Amount of attempted transfer

- Amount of payment received

- Payment channel used for attempted transfer

Anytime authorization is obtained by phone call, a recording of the call must be kept.

Solution 1: AWS S3 document storage

One way that LoanPro helps you to stay compliant is through AWS S3 Document Storage. The S3, or Simple Storage Service, is where LoanPro will put any uploaded documents for long term storage, and it is ideal for record retention. All of your records can be retained compliantly for as long as you remain a customer of LoanPro; that goes for the documents that need to be in tabular format, too. As long as documents are uploaded in the correct format, you'll never need to worry about your compliance in regards to record keeping. Additionally, the S3 is easily accessible and well organized.

Solution 2: audit trail

LMS automatically keeps many records. The primary features that show transaction and historical records are system notes and daily snapshots, which together form a detailed audit trail. Through the system notes, a lender can track all actions taken within the system, including:

- which user performed the action

- the IP address where the action was performed

- the time and date the action was taken

- what the action was

- what the action specifically did

- which entity the action was performed on

The historical loan archives, on the other hand, keep a log of specific account information each day that an account exists, which includes any custom fields a lender elects to include. These features are always running within the system and available for you to access.

Notice templates

These templates are for you; HTML versions are available for download below, and they have been created to be customizable for your company with some small tweaking. Each of our custom forms have been modeled after the CFPB's notices to ensure compliance. While the CFPB does not require lenders to use their notice layouts, deviating too much from the requirements may result in fines. Thus, we encourage you to use them.

Once you have downloaded our custom forms templates, setting up trigger-based notifications will automate the process of sending the notices to your customers. The triggers are based on rules that you set within LoanPro, and they are customizable. If you are intimidated by the prospect of creating rules, or your lending model is more complex than typical, reach out to your customer success specialist—we'd be happy to help with this process.

With the use of trigger-based notifications, we can also help you notify your customers by mail. LoanPro's mail hWhatouse tool will automatically send your notices by mail when a loan fits the criteria set by rules. Using a combination of our tools ensures you remain compliant with the CFPB's regulations with little involvement from you or your company.

When using any of the HTML templates listed below in LoanPro's custom form editor, make sure to paste the HTML text in the source code entry box. You can do so by clicking the source code button (a pair of arrow brackets < >) as shown in the screenshot below.

There are three events that you need to notify borrowers about: the first time that you initiate a withdrawal, an unusual withdrawal, and two consecutive failed payments. The CFPB's regulations allow for notices to be sent in short-form as long as they include a link to the full notice. These are referred to as Electronic Short Notices. You may want to use these to send a disclosure via a mobile app or text message. We will include examples of these with each of the full notices.

First payment withdrawal notice

Lenders are required to notify borrowers when they obtain payment withdrawal authorization. Notices can be sent in several ways, and each method has a different set of timeframe requirements. If you plan on creating your own notice, all First Payment Notices require the following content:

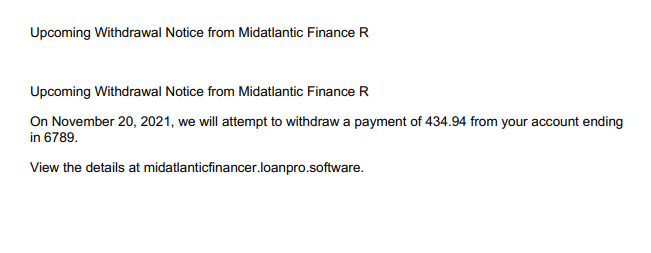

- Identifying statement (phrased exactly as "Upcoming Withdrawal Notice" with the name of the lender)

- Transfer terms (including the date, dollar amount, borrower account, loan identification number, payment channel, and check number)

- Payment breakdown (including the phrase, "Payment Breakdown" as a heading; principal, interest, fees, and other charges; the phrase "Total Payment Amount" and total dollar amount; and explanation of interest-only or negatively amortizing payment)

- Lender name and contact information

Below is an example of how the First Payment Withdrawal Notice should be formatted.

Download the HTML File for the First Withdrawal Notice

And here is an example of the Electronic Short Notice version of the First Payment Withdrawal Notice.

Download the HTML File for the First Withdrawal Electronic Short Notice

Unusual Withdrawal Notice

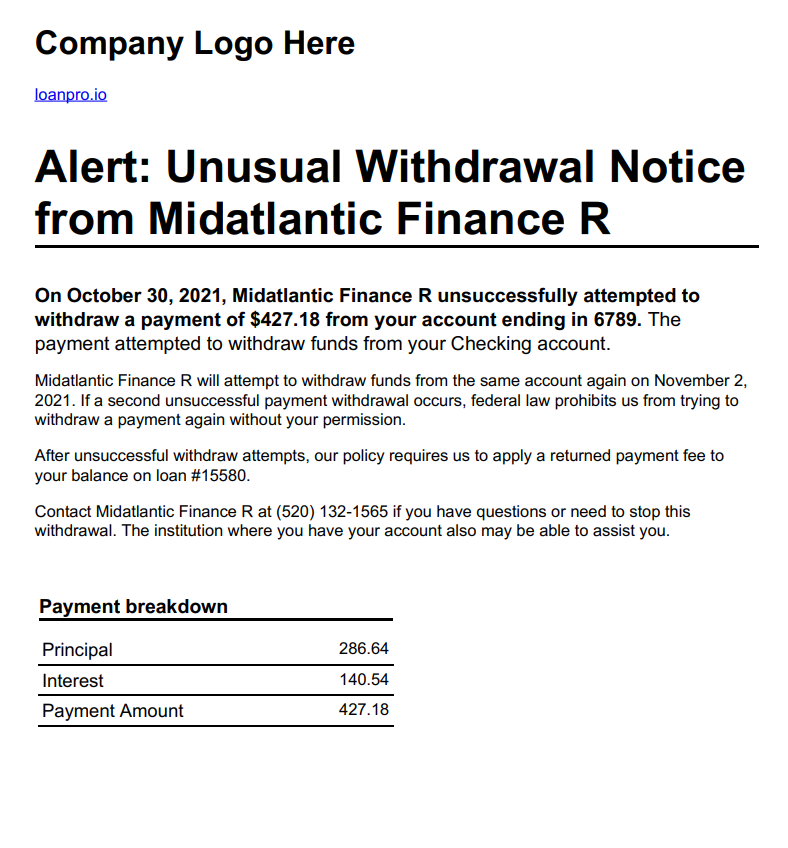

The updated regulations require lenders to notify borrowers of withdrawals that are deemed unusual. Unusual withdrawals occur when the a withdrawal does not match the previous withdrawal in some way. For example, a variation in withdrawal amount, dates, or payment channels (or, in LoanPro terms, payment profiles). The required timeframes for notice delivery vary depending on the method of notice. If you plan on creating your own notice, all Unusual Payment Notices require the following content:

- Identifying statement (including the phrase "Alert: Unusual Withdrawal" and the name of the lender)

- Basic payment information

- Description of unusual withdrawal (including varying amount, open-end credit if applicable, date other than the regularly schedule payment, different payment channel, and purpose of re-initiating returned transfer)

There are multiple variations of Unusual Withdrawal Notices. Below, we will list brief descriptions of the variations and provide examples.

Varying Amount Notice

Lenders are required to send a Varying Amount Notice when the upcoming withdrawal amount varies from the regularly scheduled payment.

Download the HTML File for the Varying Amount Withdrawal Notice

Download the HTML File for the First Withdrawal Electronic Short Notice

Different Payment Channel Notice

Lenders are required to send a Different Payment Channel Notice if the upcoming payment withdrawal will be made through a different channel (or payment profile, in LoanPro terms) than the withdrawal preceding it.

Download the HTML File for Different Payment Channel Notice

Download the HTML File for the Different Payment Channel Electronic Short Notice

Re-initiating Returned Transfer Notice

Lenders are required to send a Re-initiating Return Transfer Notice when a payment withdrawal attempt fails and the lender plans on attempting to withdraw funds again.

Download the HTML File for the Re-initiating Returned Transfer Notice

Download the HTML File for the Re-Initiating Return Electronic Short Notice

Date Other Than Due Date

Lenders are required to send a Date Other Than Due Date Notice when a payment transfer date is not on which a regularly schedule payment is due under the terms of the loan agreement. This applies to lenders who schedule withdrawal transfers a few days early to accommodate for payment processors.

Download the HTML File for the Date Other Than Due Date Notice

Download the HTML File for the Date Other Than Due Date Notice

Consumer Rights Notice

Lenders are required to send a Consumer Rights Notice to borrowers when two consecutive failed payment attempts have been made. The lender is required to send the notice no later than three business days after the second failed payment, and the notice must be made via mail, phone call, or email. The following is an example of the Consumer Rights Notice. If you plan on creating your own notice, All First Payment Notices require the following content:

- Identifying statement

- Statement of last two attempts returned

- Consumer (borrower) account

- Loan identification information

- Statement of Federal law prohibition

- Statement of contact about choices

- Previous unsuccessful payment attempts (including the phrase "previous payment attempts" as a heading, payment due date, date of attempt, amount, and fees)

- CFPB information

Both the Consumer Rights Notice and the Re-initiating Return Transfer Notice involve unsuccessful payment withdrawals from a lender. The CFPB's new regulations restrict lenders from attempting to withdraw funds from an account without permission from the borrower after two consecutive unsuccessful attempts. If you have the Retry AutoPays setting turned on, which automatically retry to withdraw funds after an unsuccessful transfer, you will need to turn it OFF to retain compliance. You can do so by navigating to Settings > Defaults > Tools > AutoPay Defaults and selecting ‘Edit’.

Below is an example of how a Consumers Rights Notice should be formatted.

Download the HTML File for the Consumer Rights Notice

Download the HTML File for the Consumer Rights Electronic Short Notice

Was this article helpful?

Unclassified Public Data