Table of Contents

Introduction

Even though you're reading an intro article, you likely understand the basic concept of bankruptcy. Bankruptcy is a legal way to absolve a borrower of debt. After that, things get fuzzy for most people. There are several types of bankruptcy, each referenced by the chapter of the US Code which they appear in. This article will go over how bankruptcy works at a basic level.

Our article Bankruptcy explains in detail how the software can help track bankruptcies.

Agent Walkthroughs Use Case

Use Cases: Process Wizards/Efficiency

The Problem

During the life of a loan, a borrower may declare bankruptcy. This process includes several steps, and can be quite involved. It also doesn't come up that often, so it probably requires special training and knowledge about all the moving parts. If a bankruptcy isn't handled correctly, it's possible the lender will lose their claim to repayment of the debt. So, it's important to make sure bankruptcy or other less-common lending processes are something that servicing agents and managers are trained on. It's also important not to let untrained personnel make uninformed bankruptcy decisions. Walkthroughs help solve these issues.

LoanPro's Solution

Lenders create Walkthroughs for lending processes, like bankruptcy, so they can give permission only to specific servicing agents to carry out those processes. Lenders can also set rules to check that a loan qualifies for a process before it's carried out. When agents use a Walkthrough they are guided through a screen-by-screen process within LoanPro that lets them enter only relevant information for each step. Each screen within the Walkthrough includes customizable, detailed instructions. Any important updates to a loan that should be made as part of the process are done behind the scenes by the Automation Engine, moving decision making to the business level and reducing training time and cost as well as human error.

Highlights

While most people think of bankruptcy as a way to get rid of debt, some types of bankruptcy are just a legal restructuring of debt. This usually means that courts will compel debtors to accept lower interest rates and payment amounts than they originally contracted to receive when the debt was issued.

Debt that Bankruptcy Won't Remove

Some types of debt are also immune to bankruptcy. These include:

- Debts that you left off your bankruptcy petition, unless the creditor actually knew of your filing

- Many types of taxes

- Child support or alimony

- Attorneys’ fees for child custody or support

- Fines or penalties owed to government agencies

- Student loans

- Personal injury debts arising out of a drunk driving accident

- Debts arising out of tax-advantaged retirement plans

- Condo or cooperative housing fee debts

- Criminal restitution and other court fines or penalties

Bankruptcy Types

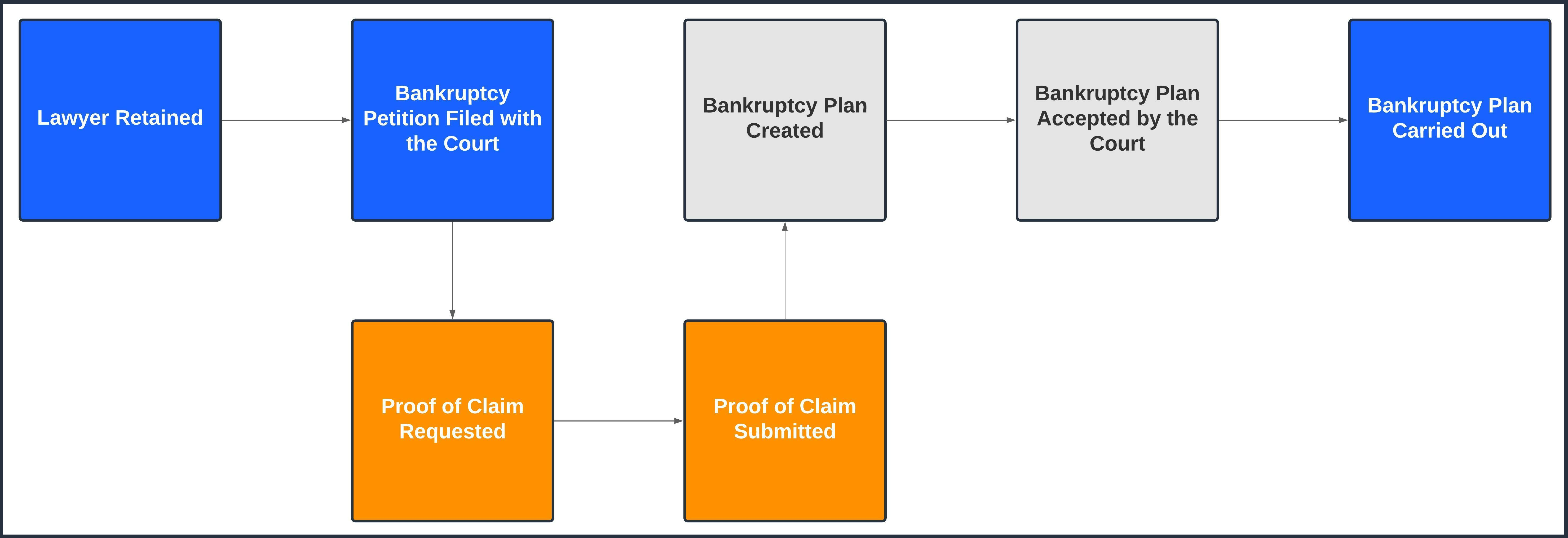

When someone chooses to declare bankruptcy, the first step is usually to contact a lawyer and discuss what the options are. There are several types of bankruptcy that are referred to by the chapter of the US code in which they appear. These include:

- Chapter 7: Bankruptcy to remove debts

- Chapter 9: Bankruptcy for Municipalities

- Chapter 11: Bankruptcy to restructure a company or personal estate if debts are above chapter 13 limits

- Chapter 12: Bankruptcy for Family Farmers

- Chapter 13: Bankruptcy to restructure debts through a repayment plan

- Chapter 15: Bankruptcy Type to Work with Cross-Border Insolvency

Chapter 7 and Chapter 13 bankruptcy are the most common. When most people hear the term 'bankrupt.,' they are most likely to thinking of Chapter 7 bankruptcy.

Bankruptcy Process

To declare bankruptcy, a petition must be filed with the courts with a list of included debt obligations. The debtor can choose to reaffirm a debt, which means they choose to keep paying the debt according to the original terms. This is often done when a collateral asset is securing the debt, because the asset (think car, house) would otherwise be taken away.

The courts will contact creditors to request a proof of claim. This is usually a form that includes specifics about the debt, but there are also requests for supporting documentation like a contract.

Once proof of debt is provided, the court will review the debts and create a plan. The plan may wipe out debts or restructure them. There is usually a proceeding attended by the debtor and creditors where the plan is presented.

Documentation explaining the plan is sent to the parties involved. If the bankruptcy involves a restructuring, the debtor will pay his new debt obligation through the bankruptcy lawyer, who will remit payment to the various creditors. If the debtor fails to pay, the bankruptcy will be dismissed, meaning the debts are all still owed according to the pre-bankruptcy terms.

If the debtor completes the payment plan, the courts will rule the bankruptcy officially discharged, meaning the obligations under the bankruptcy were met.

Where Does Bankruptcy Fit?

Declaring bankruptcy can be a complicated and meticulous process. If a borrower declares bankruptcy, a servicer needs to know how to manage the files and claims so that the process runs smoothly from start to finish. How it is managed can be a determining factor in whether or not the lender can receive a repayment of the debt.

LoanPro has a variety of tools such as Agent Walkthroughs and the ability to track bankruptcies that can help make this lending process a lot easier and manageable.

What’s Next?

Now that you understand a bit more about how bankruptcies work, check out our Bankruptcy and Default Bankruptcy Process articles to learn more about how you can use LoanPro with bankruptcies.

Written by Andy Morrise

Updated on September 10th, 2024